Housing Affordability

What This Actually Shows

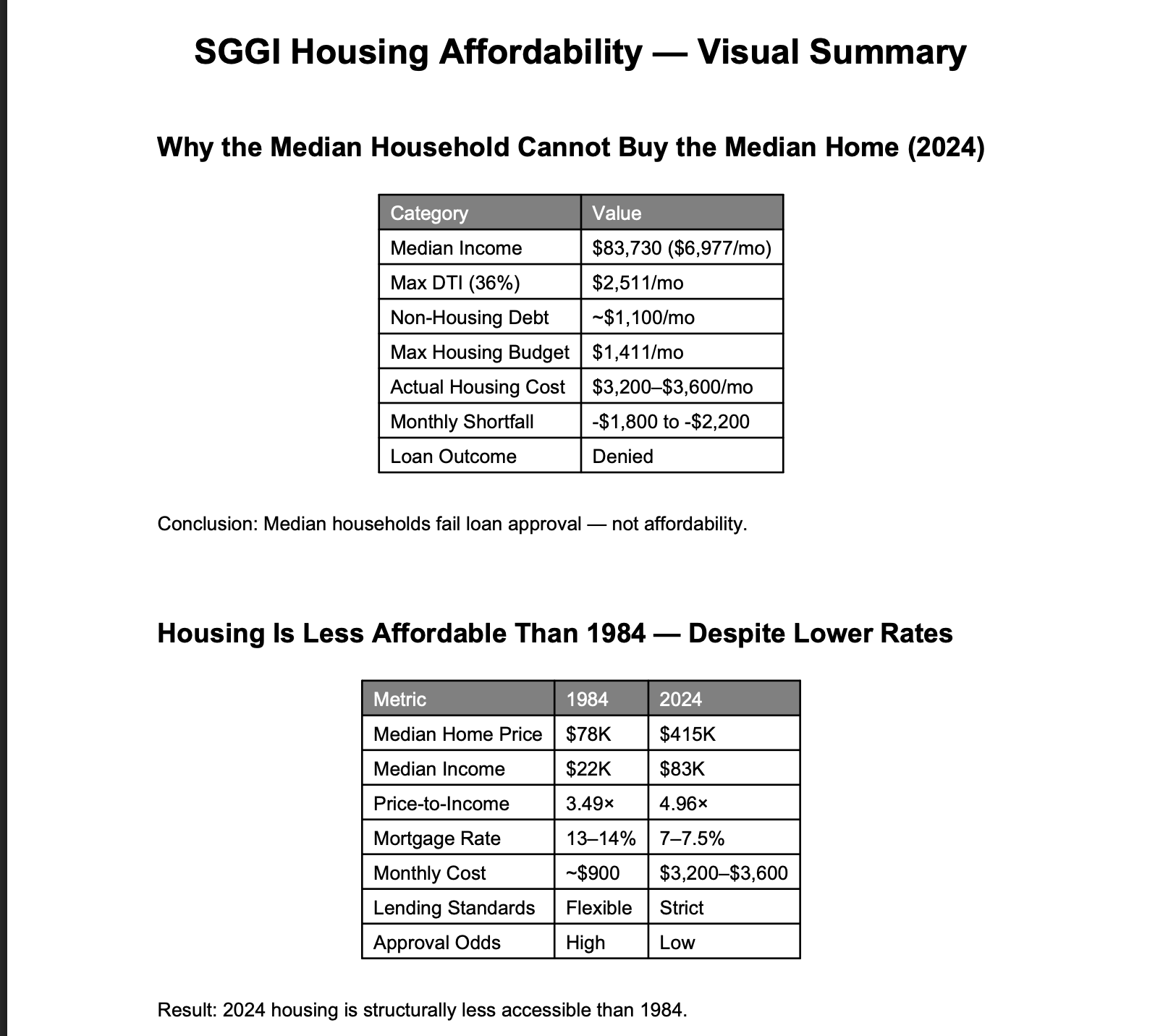

The charts above highlight something most housing discussions miss.

This is not a pricing problem.

It’s an access problem.

At a surface level, housing looks expensive because rates are high and prices haven’t come down. That’s true — but incomplete. The more important issue is that the median household cannot qualify for a mortgage on the median home, even before considering lifestyle or savings.

The first table shows the mechanical failure.

A median household earning ~$83K can support roughly $1,400/month in housing costs after accounting for existing debt and standard lending thresholds. The actual cost of the median home sits closer to $3,200–$3,600/month.

That gap — nearly $2,000 per month — is not marginal. It is disqualifying.

And importantly, this is not a question of willingness to pay. Even if a household could stretch to make the payment, modern underwriting systems won’t allow it. Debt-to-income caps, automated approval models, and higher baseline debt loads effectively block access before affordability is even tested.

That’s the structural break.

The second table explains why this cycle feels worse than prior periods — including 1984, when mortgage rates were nearly double today’s levels.

Despite 13–14% rates in 1984, housing was still more accessible because:

Prices were lower relative to income

Consumer debt burdens were minimal

Lending standards were flexible and human-driven

Today, all three have reversed.

Prices have outpaced income by roughly 40%.

Debt has moved from optional to embedded.

And lending has shifted from flexible to rule-based and automated.

The result is a system where lower interest rates no longer guarantee accessibility.

This matters for how the housing market resolves.

Traditional narratives assume relief comes from falling rates. In reality, rate cuts alone are unlikely to restore affordability at the median level. Without meaningful income growth or price declines, the qualification gap remains.

That creates a different kind of market dynamic:

Demand exists, but is locked out

Supply remains constrained

Transactions slow

Prices become sticky rather than elastic

In other words, the market doesn’t clear — it stalls.

From an SGGI perspective, housing is one of the clearest real-world examples of a broader theme showing up across the economy:

Systems where demand, capital, and physical constraints are no longer aligned.

In AI infrastructure, that misalignment shows up as power limits and delayed ROI.

In housing, it shows up as loan denial despite theoretical affordability.

Different sectors — same structure.

And until that structure resets, the constraint doesn’t disappear, it just becomes the baseline.